Movie

Movie 3 months ago

91

3 months ago

91

Getty Images

Getty Images

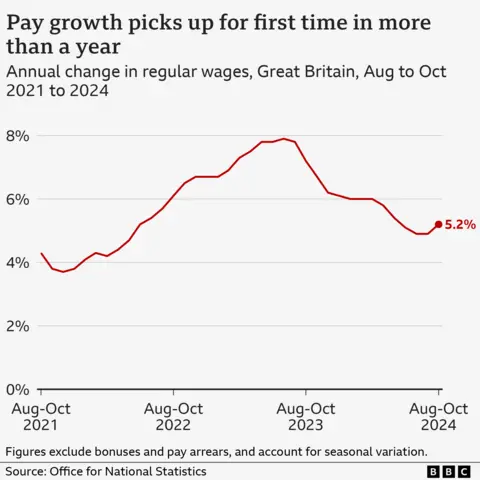

Pay growth has picked up for the first time in more than a year, according to the latest official figures.

Regular pay grew at a faster-than-expected annual pace of 5.2% between August and October, the Office for National Statistics (ONS) said.

Wages are continuing to increase faster than the price of goods. Analysts say this means the Bank of England is unlikely to cut interest rates when it meets this week.

Other figures suggested the jobs market is weakening, with job vacancies falling again and a drop in the number of people on payrolls.

The unemployment rate was unchanged at 4.3%, although there are questions over the reliability of the jobs figures from the ONS due to issues with how it gathers the data.

"After slowing steadily for over a year, growth in pay excluding bonuses increased slightly in the latest period driven by stronger growth in private sector pay," said Liz McKeown, director of statistics at the ONS.

Private sector pay grew at an annual pace of 5.4%, the ONS said.

The Bank of England has cut interest rates twice this year as price pressures in the economy have eased. However, it is not expected to make a further cut when it meets later this week.

"The latest UK jobs report provides yet more justification, if any were needed, for the Bank of England to keep rates on hold at its meeting this week," said James Smith, developed markets economist at ING.

Mr Smith noted that the jump in wage growth was entirely down to the private sector.

"This matters for the Bank, because private sector pay trends tend to be more reflective of the wider situation in the jobs market than in the public sector," he said.

The number of job vacancies fell by 31,000 to 818,000 in the September-to-November period, the ONS said, although the total remains above pre-pandemic figures.

The ONS also said provisional data indicated that the number of staff on payrolls fell by 35,000 in November 2024, although some analysts said this figure is volatile and can be subject to large revisions.

Many firms have argued the increase in employers National Insurance Contributions announced in the Budget will hit jobs.

At the weekend, the boss of Reed, one of the UK's largest recruitment firms, told the BBC the economy was "cooling", suggesting a recession may be "around the corner".

A separate survey released on Monday indicated that private sector employment December had fallen at the fastest rate for nearly four years.

Work and Pensions Secretary Liz Kendall said: "Today's figures are a stark reminder of the work that needs to be done.

"To get Britain growing again, we need to get Britain working again – so people have good jobs which pay decent wages and offer the chance to progress."

Sign up for our Politics Essential newsletter to read top political analysis, gain insight from across the UK and stay up to speed with the big moments. It'll be delivered straight to your inbox every weekday.

![Presidents Day Weekend Car Sales [2021 Edition]](https://www.findthebestcarprice.com/wp-content/uploads/Presidents-Day-Weekend-car-sales.jpg "Presidents Day Weekend Car Sales [2021 Edition]")

English (United States)

English (United States)